Mortgage Mis-selling: What You Need To Know

October 5, 2021

Customers who Believed Were Mis-sold a Mortgage are Qualified to Claim

Almost all people in UK have mortgages and this is the largest debt that many of us have. Some are satisfied with their terms and rate but most are suffering from mortgage mis-selling. There are governing laws and regulations on how mortgages are sold to consumers. When you took out your mortgage and those rules were broken, then there must be a mis-selling that happened and you could be due to compensation to mend any financial distress or suffering as a result of mis-selling.

What scenarios are considered as mortgage mis-selling?

- When the mortgage lender or broker failed to advise or give the full information about your mortgage terms and agreement.

- When the mortgage lender or broker failed to do affordability checks and assessment if you could afford the mortgage repayments.

- When the mortgage lender or broker failed to give you an array of options and encouraged you to sign up for something that is not suitable for you.

- When the mortgage lender or broker failed to give you the transparency of the fees you will be charged and how these would be paid.

- When the mortgage lender charged you with unfair and hidden fees.

What you need to know regarding mis-sold mortgage that you need stay away from:

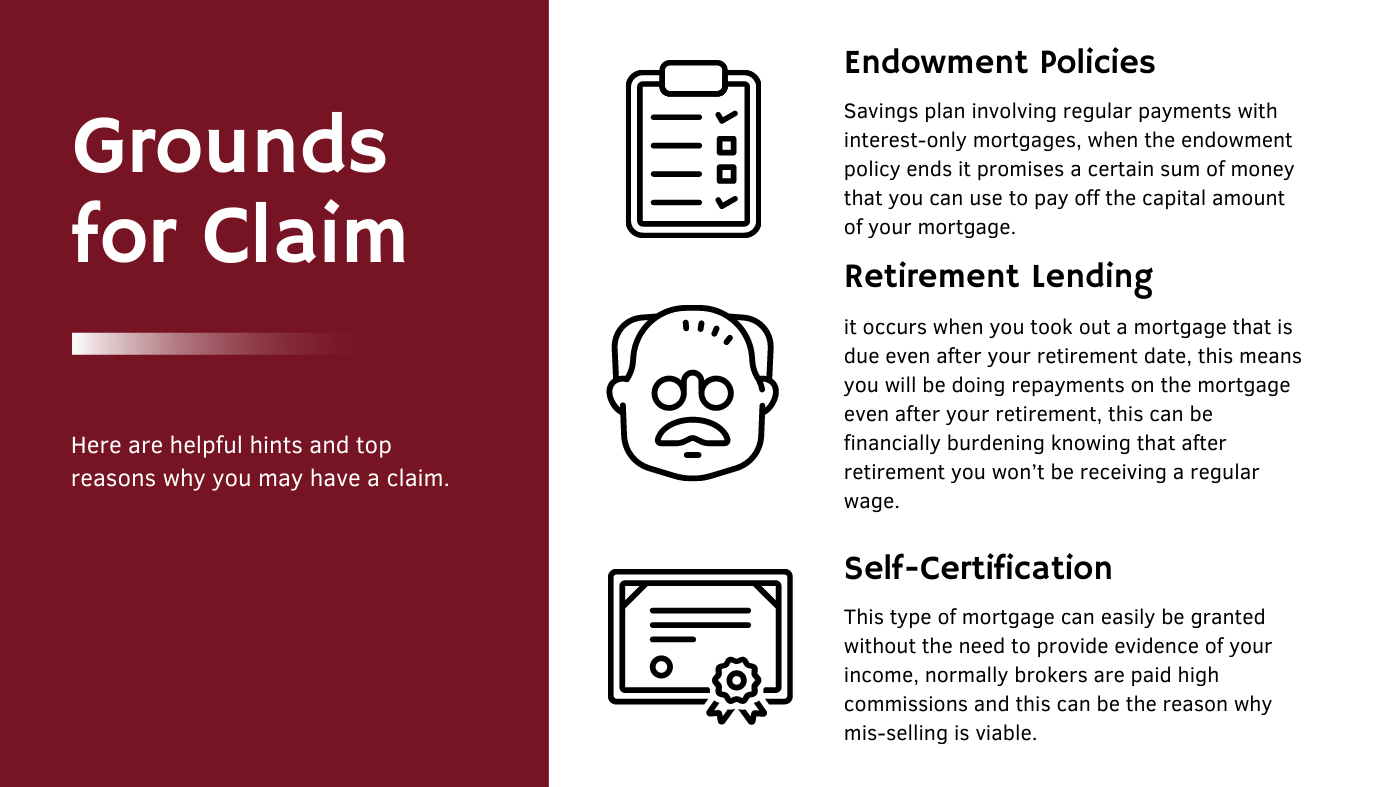

- Endowment policies - savings plan involving regular payments with interest-only mortgages, when the endowment policy ends it promises a certain sum of money that you can use to pay off your capital amount of your mortgage.

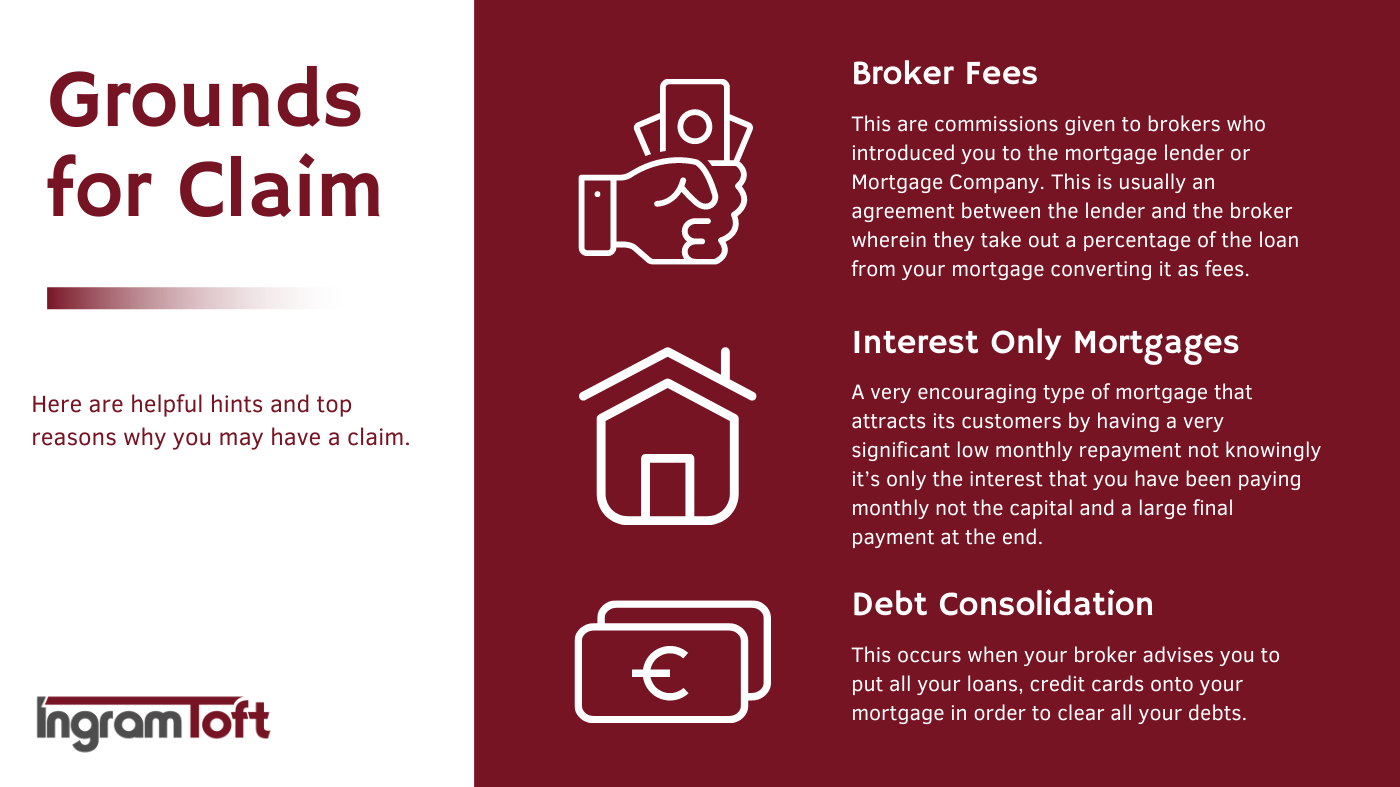

- Interest Only Mortgages – a very encouraging type of mortgage that attracts its customers by having a very significantly low monthly repayment not knowingly it’s only the interest that you have been paying monthly not the capital and a large final payment at the end.

- Fast-track or self-certification mortgages – this type of mortgage can easily be granted without the need to provide evidence of your income, normally brokers are paid high commissions and this can be the reason why mis-selling is viable.

- Broker Fees – this are commissions given to brokers who introduced you to the mortgage lender or Mortgage Company. This is usually an agreement between the lender and the broker wherein they take out a percentage of the loan from your mortgage converting it as fees which means you have been paying interests without your knowledge.

- Mortgage beyond retirement age – it occurs when you took out a mortgage which is due even after your retirement date, this means you will be doing repayments on the mortgage even after your retirement, this can be financially burdening knowing that after retirement you won’t be receiving a regular wage. This should be discussed with you in transparency before taking out the mortgage to make sure you can meet the required repayments even after retirement.

- Remortgaging to Clear or Consolidate Debts – this occurs when your broker advises you to put all your loans, credit cards onto your mortgage in order to clear all your debts.

Those mentioned above are examples are helpful hints to give you the common scenarios and situation when a mortgage mis-selling may occur. If you have experience any of the above examples, gather all the information regarding your mortgage and get in touch with our team of claim experts so we can look into this for you and build a strong compelling case for a mis-sold mortgage compensation.

Have you or someone you know been a victim of a romance scam? It can be a painful and isolating experience, but help is available. At [Your Company Name], we specialize in supporting victims of online romance fraud by offering professional guidance to help recover lost funds. Our team understands the complexities of these scams and is committed to assisting you every step of the way toward compensation and peace of mind. Don’t let scammers get the last word—reach out to explore your options for financial recovery today

Discover 30 expert tips to protect your finances from cryptocurrency scams in the UK. Our comprehensive guide covers the essentials of cryptocurrency, identifies common types of crypto frauds, and provides actionable advice to shield yourself from these scams. Whether you're a novice or an experienced crypto user, learn how to safeguard your digital assets and navigate the process of claiming compensation if you fall victim to a scam. Stay informed and secure in the ever-evolving world of cryptocurrency.

Failure of FTX crypto exchange